Imagine two neighbors, Sarah and James. Both worked for 35 years, saved diligently in their 401(k) plans, and retired with exactly $1 million in their accounts. Both followed the classic “4% rule,” withdrawing $40,000 in their first year of retirement and adjusting for inflation thereafter. Over their 25-year retirements, the stock market provided both of them with an identical average annual return of 7%.

Fast forward two decades: Sarah is traveling the world with a portfolio that has grown to $1.8 million. James, however, is terrified of outliving his money because his balance has plummeted to less than $200,000. How can two people with the same savings, the same withdrawal rate, and the same average market returns end up with such drastically different results? The answer lies in a phenomenon called sequence of returns risk.

Sequence of returns risk is the danger that the order of your investment returns—specifically receiving poor returns in the early years of retirement—will permanently damage your portfolio’s ability to support you. While “average” returns matter during your working years, the actual “sequence” of those returns becomes the most critical factor the moment you start withdrawing money.

The Math Behind the Risk: Why Averages Lie

During your wealth-building years, the order of returns doesn’t matter. If you are only contributing money and not taking any out, a 20% drop in year one followed by a 20% gain in year two results in the same final balance as a 20% gain followed by a 20% drop. This is due to the commutative property of multiplication; the order of the numbers you multiply doesn’t change the product.

Everything changes when you introduce cash outflows. When you withdraw money from a declining account, you liquidate more shares to meet your spending needs. This effectively “locks in” your losses. You are no longer giving those shares the opportunity to participate in the eventual market recovery. You are essentially cannibalizing your seed corn during a drought, leaving you with nothing to plant when the rain finally returns.

To understand the gravity of this, consider the following comparison of two hypothetical investors over a 10-year period. Both start with $1,000,000 and withdraw $50,000 annually (inflation-adjusted at 3%).

| Year | Market Return (Lucky Larry) | Market Return (Unlucky Ursula) |

|---|---|---|

| 1 | +20% | -15% |

| 2 | +15% | -10% |

| 3 | +10% | -5% |

| 4 | +5% | +5% |

| 5 | 0% | 0% |

| 6 | 0% | 0% |

| 7 | -5% | +5% |

| 8 | -10% | +10% |

| 9 | -15% | +15% |

| 10 | -20% | +20% |

| Avg Return | 0% | 0% |

Even though their average returns are identical, Lucky Larry—who saw gains early on—will have a significantly higher balance after year 10. Unlucky Ursula, who faced a market crash at retirement, had to sell shares at rock-bottom prices just to pay her bills. Her portfolio may never recover, even when the market eventually turns positive.

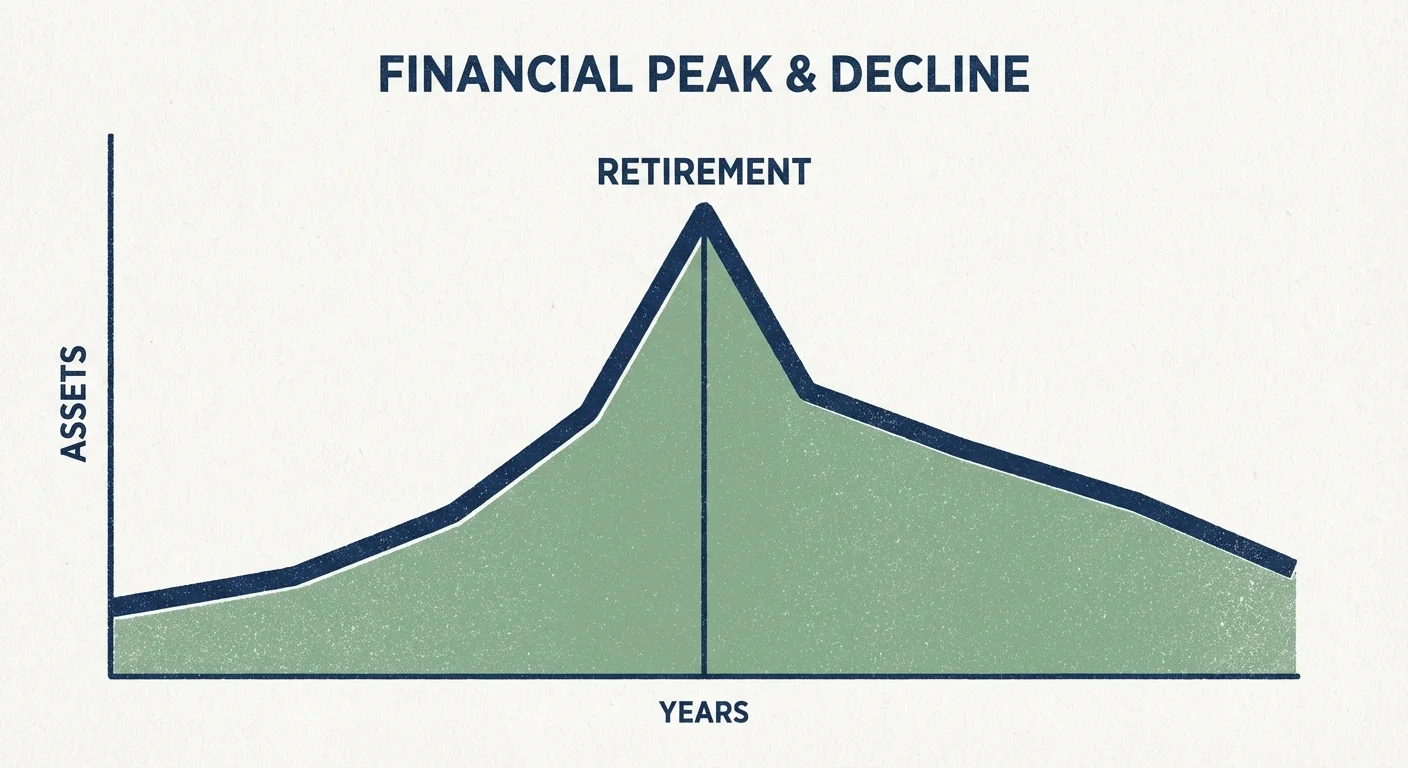

The Retirement Red Zone

Financial planners often refer to the five years immediately preceding and the five years immediately following your retirement date as the “Retirement Red Zone.” This decade is the period of maximum vulnerability. During this window, your portfolio is likely at its largest size, and you are transitioning from a “saver” to a “spender.”

A significant market downturn during this period creates a mathematical hurdle that is nearly impossible to clear. If you lose 30% of your portfolio right as you retire, you don’t just need a 43% gain to get back to even. Because you are also withdrawing 4% or 5% for living expenses, you might actually need a 60% or 70% gain just to regain your original starting point. This is why retirement timing feels like a gamble—but it doesn’t have to be.

“The stock market is a giant distraction from the business of investing.” — John Bogle, Founder of Vanguard

As Bogle suggested, focusing on the noise of daily fluctuations can lead to panic. However, sequence of returns risk is not just “noise”—it is a structural threat to your financial plan that requires a proactive defense strategy.

Defensive Strategy 1: The Cash Bucket Approach

One of the most practical ways to combat sequence risk is to change where you pull your money from during a down market. Instead of selling stocks when they are low, you maintain a “cash bucket” or “liquidity reserve.”

Under this strategy, you keep two to three years of living expenses in highly liquid, non-volatile accounts, such as high-yield savings accounts or money market funds. When the stock market is performing well, you refill this bucket with your capital gains. When the market crashes, you stop selling stocks entirely and live off your cash reserve. This gives your equity portfolio the time it needs—usually three to five years—to recover without being depleted by forced liquidations.

You can find more information on managing your cash and investment accounts through resources like FINRA’s Investor Education pages, which detail how different account types function during market shifts.

Defensive Strategy 2: Dynamic Spending and Guardrails

The “4% Rule” is a helpful benchmark, but it is often too rigid for the real world. A more resilient approach is dynamic spending, also known as the Guyton-Klinger rules. This strategy involves setting “guardrails” for your withdrawals based on market performance.

If your portfolio value drops significantly, you reduce your spending by a predetermined amount (e.g., 10%) for that year. Conversely, if your portfolio performs exceptionally well, you might grant yourself a small raise. By reducing your “burn rate” during lean years, you preserve more of your principal, allowing it to compound more effectively when the market rebounds. This flexibility is your greatest weapon against a poor sequence of returns.

Defensive Strategy 3: The Bond Tent

A “Bond Tent” is a tactical asset allocation strategy specifically designed for the Retirement Red Zone. Most investors believe they should gradually increase their bond exposure as they age. However, the Bond Tent suggests you should reach your peak bond allocation on the day you retire, and then actually increase your equity exposure over the next 10 to 15 years.

- Phase 1: 5-10 Years Before Retirement. Slowly decrease your stock exposure and increase your bond exposure. If you usually keep a 60/40 stock-to-bond ratio, you might move toward a 40/60 ratio by your retirement date.

- Phase 2: The First 10 Years of Retirement. Use your bond holdings to fund your lifestyle while leaving your stocks untouched. As you spend down the bonds, your percentage of stocks naturally rises.

- Phase 3: Mid-Retirement. You eventually return to a more standard 60/40 or 50/50 allocation.

The goal of the tent is to provide maximum protection during the years when you are most vulnerable to a market crash. By the time you are 15 years into retirement, sequence risk has naturally diminished because your “time horizon” for the remaining funds has shortened.

Maximizing Guaranteed Income Sources

The more of your floor expenses (housing, food, utilities) you can cover with “guaranteed” income, the less you have to rely on your volatile investment portfolio. This significantly lowers your exposure to sequence of returns risk.

For most Americans, Social Security is the primary tool for this. Delaying your Social Security benefits is one of the most effective hedges against market volatility. For every year you delay taking benefits past your Full Retirement Age (up to age 70), your monthly check increases by approximately 8%. This is a guaranteed, inflation-adjusted “return” that no market investment can match. You can estimate your future benefits by creating an account on the Social Security Administration (SSA) website.

If you have a pension or choose to purchase a simple immediate annuity, these also serve as stabilizers. When the market drops 20%, your Social Security check and pension stay exactly the same. This allows you to keep your hands off your 401(k) and IRA during a downturn.

Avoiding Common Errors

Even the best-laid plans can fail if you succumb to emotional decision-making. Avoid these common pitfalls that exacerbate sequence of returns risk:

- Panic Selling: Selling your entire portfolio and moving to cash after a 20% drop is the fastest way to ruin a retirement. It turns a “paper loss” into a permanent loss and ensures you miss the recovery.

- The “Yield Chase”: When interest rates are low, many retirees move into “high-dividend” stocks or “junk bonds” to generate income. These assets often crash exactly when the broader market does, providing no protection when you need it most.

- Ignoring RMDs: Once you reach age 73 (or 75 depending on your birth year), the IRS requires you to take Required Minimum Distributions (RMDs). If the market is down, you are forced to withdraw money, which can trigger sequence risk. Plan your tax strategy early to mitigate this impact. You can check the latest RMD tables and rules on the Internal Revenue Service (IRS) website.

- Over-withdrawal in Good Years: It is tempting to spend more when the market is up 25%. However, those “buffer” years are what sustain you during the “lean” years. Stick to your spending plan.

The Role of Housing Equity

For many retirees, their home is their largest asset. While usually considered “illiquid,” housing equity can serve as a backstop against sequence of returns risk. In a severe multi-year bear market, some retirees use a Home Equity Line of Credit (HELOC) or a reverse mortgage (for those over age 62) to fund their lifestyle temporarily. This allows the investment portfolio to remain untouched until prices recover. However, these tools carry costs and risks, so you should research them thoroughly on sites like the Consumer Financial Protection Bureau (CFPB) before proceeding.

When DIY Isn’t Enough

While many people can manage their own retirement, certain scenarios make sequence of returns risk too complex to handle alone. You might want to seek professional guidance if:

- You are retiring with a “lean” portfolio. If your withdrawal rate is higher than 4.5%, your margin for error is razor-thin. A professional can help you stress-test your plan.

- You have complex tax considerations. If you have a mix of Roth, Traditional, and taxable brokerage accounts, the order in which you tap these accounts (tax-bracket management) can significantly impact how long your money lasts.

- You are facing a “Black Swan” event. If a major market crash coincides with an unexpected health crisis or family emergency, the emotional toll can make objective decision-making impossible.

- You are unsure about Social Security timing. The “optimal” time to claim Social Security depends on your health, your spouse’s needs, and your other assets. A specialized analysis can often find tens of thousands of dollars in “hidden” lifetime benefits.

Frequently Asked Questions

Is sequence of returns risk the same as market risk?

Not exactly. Market risk is the general chance that your investments will lose value. Sequence of returns risk is the specific risk that those losses occur at the worst possible time—the beginning of your withdrawal phase. A market crash 20 years into retirement is much less dangerous than a crash in year one.

Can I avoid this risk by only investing in bonds?

While bonds are less volatile, an all-bond portfolio carries “inflation risk” and “interest rate risk.” If you don’t have some exposure to stocks, your purchasing power will likely erode over a 30-year retirement. The key is balance, not total avoidance of equities.

How much cash should I really keep?

Most experts recommend keeping 12 to 24 months of “gap” income—the amount you need beyond Social Security and pensions—in a liquid account. This ensures you can weather a standard market correction without selling a single share of stock.

Does a high inflation environment make sequence risk worse?

Yes. High inflation forces you to withdraw more dollars to maintain the same standard of living. If this happens during a market downturn, the “double whammy” of high withdrawals and low returns can accelerate portfolio depletion.

Practical Next Steps

Sequence of returns risk is a mathematical reality, but it doesn’t have to be a retirement-ender. Your goal is to build a “weather-proof” retirement plan that recognizes that the market does not move in a straight line. Start by calculating your “Retirement Red Zone” dates. If you are within five years of that window, begin building your cash bucket and re-evaluating your asset allocation.

Focus on what you can control: your spending flexibility, your diversification, and your reaction to market volatility. By implementing guardrails and prioritizing guaranteed income, you ensure that your retirement is defined by your choices, not by the random luck of a market cycle.

This is educational content based on general financial principles. Individual results vary based on your situation. Always verify current tax laws, investment rules, and benefit eligibility with official sources.

Last updated: February 2026. Financial regulations and rates change frequently—verify current details with official sources.

Leave a Reply